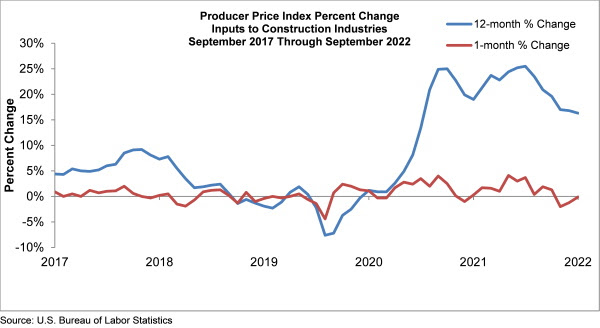

Construction input prices dipped 0.1% in September compared to the previous month, according to an Associated Builders and Contractors analysis of U.S. Bureau of Labor Statistics’ Producer Price Index data released today. Nonresidential construction input prices also fell 0.1% for the month.

Construction input prices are up 16.3% from a year ago, while nonresidential construction input prices are 15.9% higher. Input prices were down in six of 11 subcategories on a monthly basis. Steel mill prices fell 6.7% and iron and steel prices dropped 5.4%. Natural gas prices rose 3.1%, while crude petroleum prices were down 3.4% in September. Overall producer prices expanded 0.4% in September, a larger increase than the consensus estimate of 0.2%.

“Investors and other stakeholders are eagerly awaiting any indications of meaningful declines in inflationary pressures,” said ABC Chief Economist Anirban Basu. “Elevated inflation and interest rate increases have not only undone momentum in America’s homebuilding industry but also threaten the entire global economy. There are already indications of growing financial stress, including at banking giant Credit Suisse. This is bad news for the heavily financed real estate and construction segments.

“While many American nonresidential contractors remain upbeat, according to ABC’s Construction Confidence Index, there are significant threats looming over the industry,” said Basu. “Next year stands to be a weak one for the U.S. economy as it continues to absorb the impacts of rapidly rising borrowing costs.

“Today’s PPI release strongly suggests that there is no impending end to the Federal Reserve’s rate-tightening, which means that negative factors threatening the broader economy and nonresidential construction are only getting stronger,” said Basu. “While nonresidential input prices fell slightly, inflation came in hotter than anticipated in the overall report. For contractors, the upshot is that they should be actively preparing their respective balance sheets for a downturn, even as many firms presently operate at capacity.”